The phenomenon of money residence purchases turns into stronger as a result of rise in charges | Economy | EUROtoday

Two bedrooms, two loos and 80 sq. meters. It is the condo that Graciela, a 43-year-old Spanish lady, has simply purchased within the very rich Salamanca neighborhood in Madrid. She has paid 400,000 euros in money. “The money came from a donation that my parents made to me and it seemed like a good investment,” says the lady, who for privateness causes asks to not be recognized by her final identify and refuses (like the remainder of the individuals who give their testimony) to seem within the picture. . “If interest rates had been lower, I would have considered buying something larger and taking out a mortgage; But as they are, it is better to buy with what you have,” she continues.

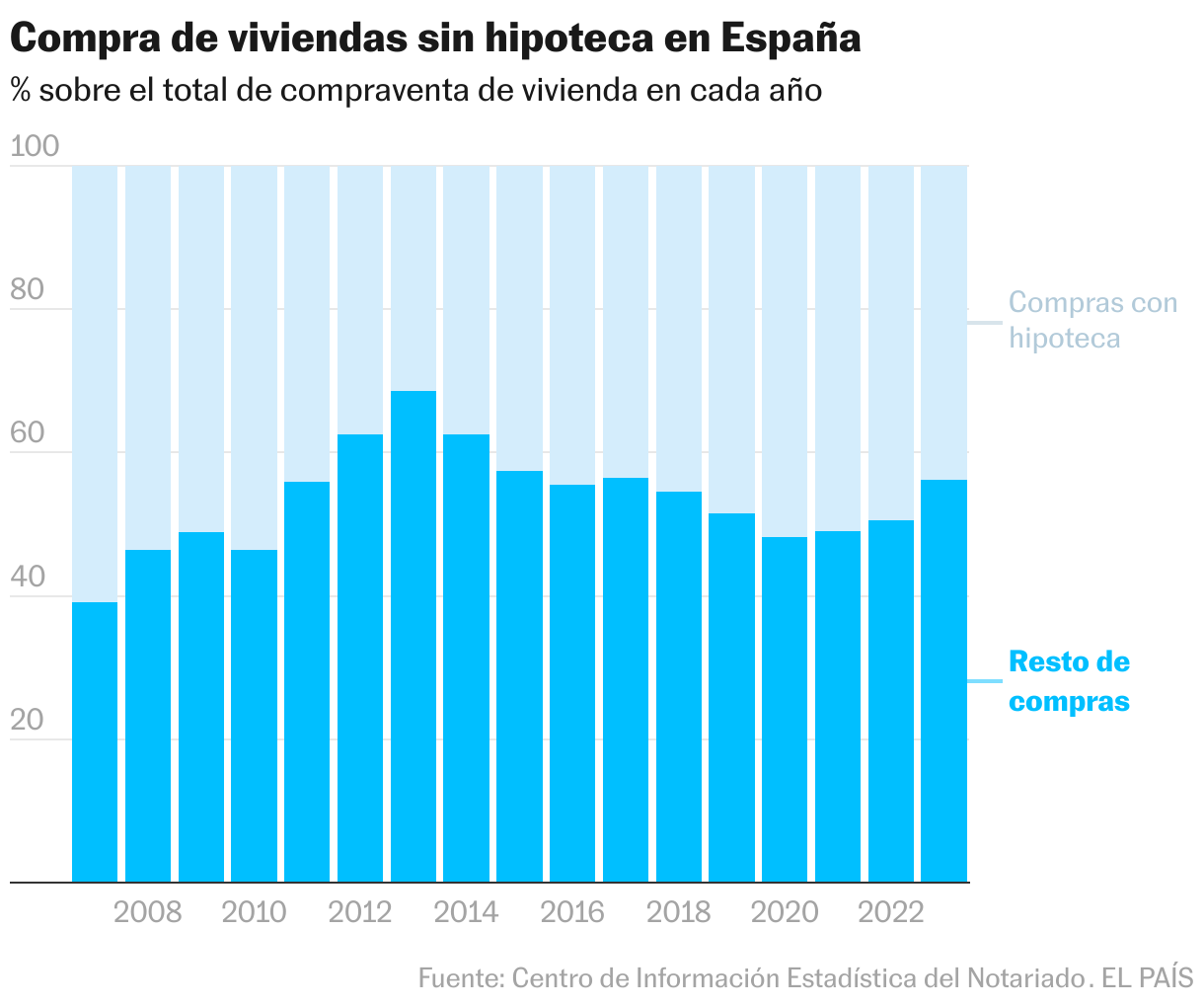

This lady's state of affairs could appear anomalous, however the knowledge says that it isn’t so anomalous. Home purchases wherein a mortgage shouldn’t be requested have gained prominence in Spain as loans have change into dearer. People who promote a home to purchase one other, traders (people or firms) and international patrons are those that are encouraging the phenomenon. This shouldn’t be new: one thing related was already seen within the disaster that adopted the bursting of the actual property bubble, nevertheless it has gained power lately. In some months, final December with out going any additional, flats paid by the bucket have come to symbolize nearly 60% of the market.

Exactly, based on the info dealt with by notaries, within the final month of 2023 the proportion of mortgages that have been supposed to accumulate a house represented 42.5% of the full variety of homes that modified fingers. In different phrases, the homes bought that didn’t have mortgage financing included represented 57.5% of the full. If we take a look at the 12 months as an entire, the proportion drops considerably, to 56%. But even so, it’s one thing unprecedented when you take a look at earlier years: 51% in 2022, 49% in 2021 and 48% in 2020.

If we take a look at the figures from the property registrars, from which the official statistics of the INE draw, these percentages are a lot much less giant as a result of this supply doesn’t discriminate housing mortgages by function. Furthermore, since registration shouldn’t be obligatory, however banks do require it to grant the mortgage, financing operations attain the registries extra often. But, to a higher or lesser extent, they comply with the identical pattern. Last 12 months, residence purchases fell by 10% and, however, mortgages fell rather more: 18%. Whichever means you take a look at it, the conclusion is similar: there is part of the actual property market that’s being sustained by operations wherein a mortgage mortgage shouldn’t be requested.

Ernesto Ferrer-Bonsoms, actual property enterprise director at Solvia, lists three causes: “The most obvious is that some buyers choose to pay in cash to save interest, take advantage of their savings or inheritances, or avoid banking requirements and procedures,” he feedback. Behind these purchases are primarily particular person traders, funds or giant firms, each Spanish and worldwide, that search to do enterprise in the actual property sector, “especially in large cities or tourist areas, where prices have a clear upward trend and have recovered investment confidence,” completes the expert.

The director of the Living Investment area (residential) at CBRE, Ofelia Núñez, agrees that the rise in bank interest rates has represented a turning point for the market. “When the cost of money was practically zero, financing helped the equation and benefited the returns,” he recalls, but now, especially in the central locations of the main cities, “the debt costs you more than the profitability it generates.” ”. That is, investors use cash to buy. Especially family companies or fortunes. “There have always been families that have invested in residential rentals,” explains the expert, “but now they are given more focus because they are more protagonists as institutional investment slows down.” [fondos y grandes compañías]”.

Interest increase

Official interest rates in the eurozone have risen to 4.5% after the ten increases carried out by the European Central Bank (ECB) between July 2022 and September of last year to try to contain inflation. This increase in the official price of money has been transferred by banks to their mortgage offers. And that makes access to housing difficult for the majority of Spanish families, who bought fewer houses last year. But those who can acquire without financial backing do not have that problem.

“Interest rates make mortgages less profitable for investors and prohibitive for those looking for a house to live in,” summarizes Héctor Tramullas, general director of Gilmar. In this real estate agency, focused on high-end homes, they are used to instant purchases, but they believe that “the trend has spread.” “In the Salamanca neighborhood we see 70% of purchases and sales without a mortgage, but here there have always been a lot of acquisitions of this type. On the Costa del Sol, where people buy with money that does not need a mortgage, there are now 60% of operations without financing, 20% more than six months ago,” says Tramullas, who describes “an increase in foreign clients, especially Latinos who are looking for a stable country in which to live, have a second residence or invest their money.”

According to data from registrars, last year the proportion of foreign buyers out of the total increased. And the majority are still Europeans, who are the usual clientele of TM Grupo Inmobiliario, specialized in second coastal homes. Daniel Sánchez, head of the firm's international commercial area, points out that among these buyers “the half that requests financing could be very low, even whether it is provided to them.” The reasons are varied: “They can obtain financing in their country or come with their own resources, it depends on the origin and the circumstances of the moment,” he says. Belgians, he exemplifies, usually ask for mortgages from their banks taking advantage of the high valuation of houses there. The Poles, on the other hand, have bought a lot in recent times as an investment due to a slowdown in their real estate sector.

When it comes to investments, the Madrid notary Alfonso Madridejos reports on a type of operation that has become common: “These are the premises that an investor buys and converts, at least, into four apartments that he rents for 800 euros per month. ”.

Sell to buy

But the weight of buyers who sell their previous home and obtain liquidity to purchase another home that better suits their needs is not negligible. Replacement purchases have always been one of the main drivers of the Spanish real estate market, especially after the pandemic. There has also been an increase in buyers bringing an inheritance under their arm or taking advantage of family loans. This profile seeks both first and second residences.

In the Tecnocasa real estate network, the percentage of homes purchased in cash was 42.3% last year. This is because they work with medium and low priced homes. The weight is lower than the record of 2014, when 56.2% of operations were carried out without a mortgage. “That year there were cheap prices and difficulties in granting credit,” says Lázaro Cubero, head of Analysis for the group. The average price of apartments purchased without financing in their offices is 133,000 euros. “Many buy to renovate and sell, to rent, to protect their money from inflation or to give it to their children,” says the analyst, who cites a significant advantage for those who can afford to pay in full: “Detect the opportunity and it is a “You purchase sooner since you don't should go to the financial institution.”

Roberto is from Malaga, he is 50 years old and three months ago he bought for 67,000 euros, in cash, a one-bedroom house with a 1,200-meter plot in Rota (Cádiz) through Tecnocasa. “I had some savings, the rates now are not the best and, being a second home, the financing is worse,” he remembers. His intention is twofold: to use the property as a second residence and as an investment. His case fits with the experience of Mayte Muñoz, director of Financial Services at Re / Max Spain: “Whoever buys their first home needs a mortgage, that client stopped in 2023,” he says. At the brand's headquarters they counted 60% of operations without financing last year.

The trend is not exclusive to Spain because the rise in financing costs has affected almost all Western countries, which in recent years have faced an inflationary crisis unknown in decades. In the US, the real estate services firm Redfin noted that last September a peak in sales without financing of 34% had been reached. In one year, the indicator rose five percentage points.

But, even though it is widespread, the new reality of the real estate market ceases to surprise. Sometimes even to those who are part of the sector, like José Luis Benítez, an agent at the Alfa Arturo Soria real estate agency in Madrid. Last year, he says, he sold 12 houses and made full payment: “100% were without a mortgage and it had never happened to us. “We haven't made any mortgage for a 12 months and a half.” 60% of his transactions have been carried out by foreigners, especially Venezuelans, Mexicans and Argentines. “They have cash, they are businessmen.” One of his last sales was that of a chalet for 1.3 million euros. And he says that it barely took him a week to close the operation: “The first time a 26-year-old Mexican girl who was studying in Madrid visited him. The following week her father came from Mexico and bought it for her as a wedding gift.”

Follow all the information Economy y Business in Facebook y Xor in our newsletter semanal

The Five Day agenda

The most important economic quotes of the day, with the keys and context to understand their scope.

RECEIVE IT IN YOUR MAIL

Subscribe to continue reading

Read without limits

_

https://elpais.com/economia/2024-02-25/el-fenomeno-de-la-compra-de-vivienda-al-contado-se-hace-fuerte-por-la-subida-de-tipos.html