The expansive cycle of the financial system and its expiration | Business | EUROtoday

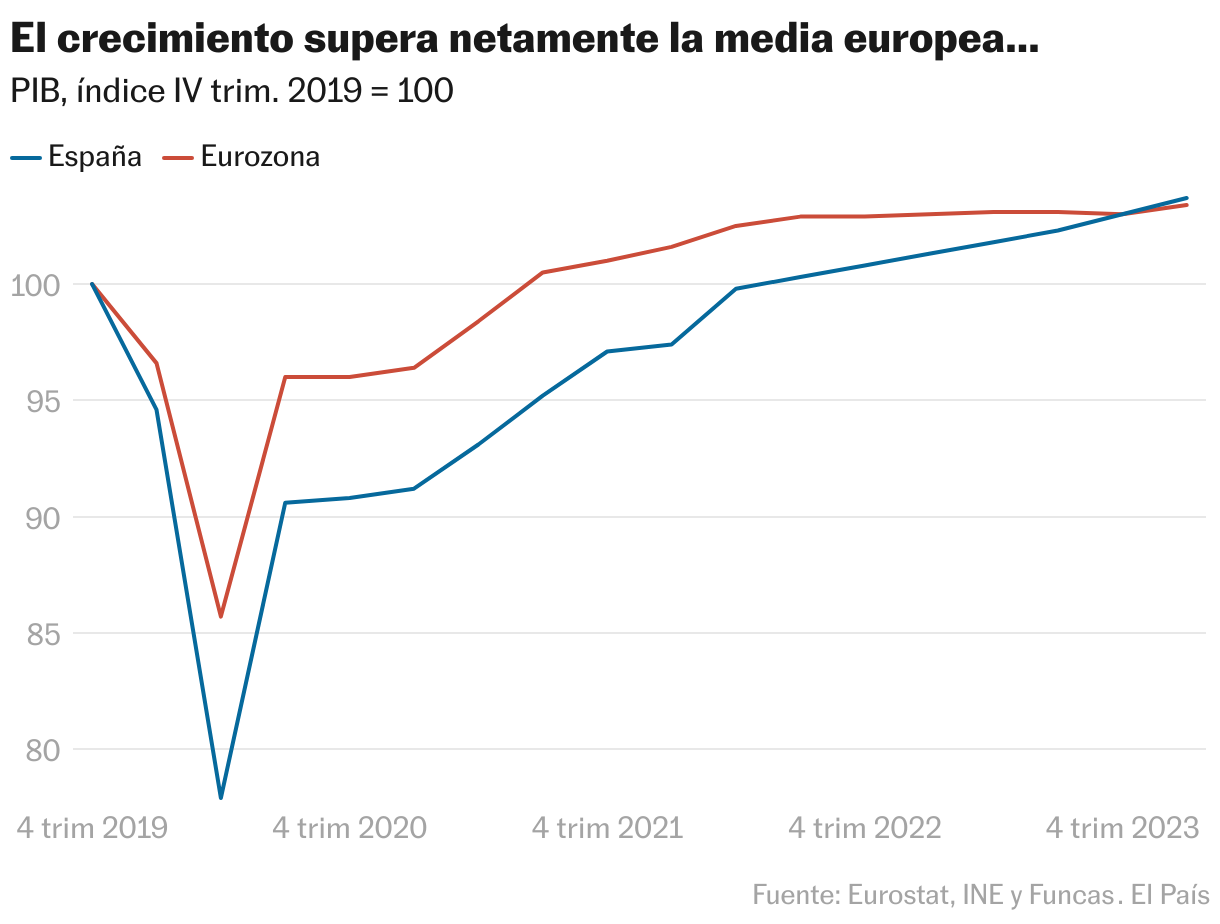

The upward streak of the Spanish financial system continues, with GDP development of 0.7% at the start of the yr, greater than double the European common. The overseas sector contributes virtually 70% of this development, the results of the increase in service exports and the slackness of imports, an element that mechanically detracts from exercise. The remaining 30% comes from home demand, this being a variable that additionally appears to evolve in a extra balanced approach: funding rebounds after the hit of the pandemic and world uncertainties, whereas the pull of public consumption dissipates. in a context of price range extension. And household consumption advantages from the rise in labor earnings.

To what extent does the Spanish financial system have the assets to maintain a balanced expansionary cycle? Some indicators are encouraging. Spain appears to have strengthened its worldwide competitiveness because of entry to considerable and low-cost power in relation to the primary neighborhood companions; to the shortening of the provision chains of huge firms, in a logic of economic blocks; and immigration, a plus for a productive mannequin primarily based on the incorporation of the workforce. However, the power disaster and geopolitical tensions, clearly dangerous within the brief time period, may have generated tectonic actions in globalization with stunning collateral results for our financial system.

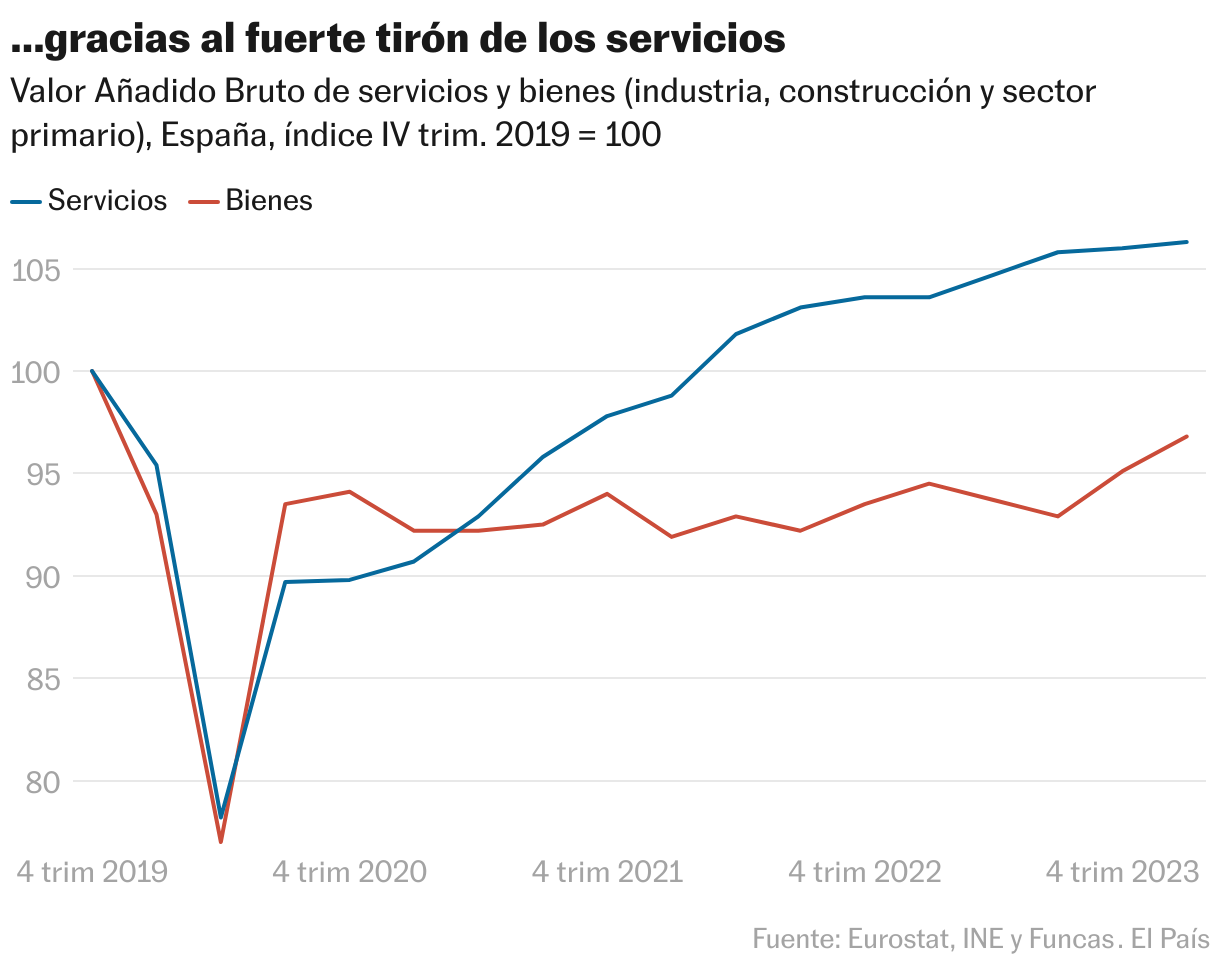

Faced with the speculation of a shock favorable provide, it’s price recognizing the function of risky elements on the demand facet, which is able to disappear sooner fairly than later. Firstly, world consumption has quickly shifted in direction of providers – with our nation being one of many fundamental beneficiaries – to the detriment of products, notably industrial ones. According to Eurostat, in comparison with the pre-pandemic scenario, European households spend proportionally extra on journey, eating places and different providers, and fewer on industrial merchandise, affected by provide issues and the power disaster.

The deviation is perceived within the Spanish financial system: the added worth of the providers sector was 6.3% above the pre-pandemic stage within the first quarter, whereas the products sector, which incorporates trade, development and branches primaries, fell 3.2%. However, shopper preferences are set to normalize as relative costs stabilize.

Secondly, the weak efficiency of imports is a largely ephemeral phenomenon, because it displays a minimum of partly the shift in demand in direction of providers, these being 4 instances much less intensive in imported inputs than items (in accordance with estimates primarily based in tables input-output, supported by a current ECB research). So it’s foreseeable that imports will recuperate as shopper preferences are restored, even bearing in mind an eventual enchancment within the share of Spanish firms within the home market.

The possible dilution of the adjustments within the sample of demand, along with the restrictive flip in fiscal coverage, will weaken the expansionary cycle, whose persistence will subsequently depend upon the persistence of the constructive provide shock, that’s, on our potential to advertise structural advances in bettering the manufacturing mannequin. The turning level ought to happen subsequent yr, when much less buoyant demand is anticipated on account of the normalization of consumption patterns, each private and non-private. The secret is to strengthen the present aggressive benefits, with funding being a mandatory situation to attain this, notably in a context of accelerated technological change. In this regard, the rebound in funding continues to be too incipient to envisage an enlargement of productive capability. And to unblock productiveness, the important thing to producing an unprecedented, however achievable, cycle of sustainable convergence with Europe.

Investment

Investment (GFCF) rose 2.6% within the first quarter of 2024 because of the restoration of capital items parts and non-residential development. Investment in housing and mental exercise merchandise, nonetheless, fell. Despite the end result achieved between January and March, funding continues to be 2.2% under the pre-pandemic stage. The funding deficit in housing reaches 8.2%, and within the case of capital items, 6.4%. Only funding in different constructions and mental property merchandise exceed this stage.

Follow all the knowledge Economy y Business in Facebook y Xor in our publication semanal

Subscribe to proceed studying

Read with out limits

_

https://elpais.com/economia/negocios/2024-05-05/el-ciclo-expansivo-de-la-economia-y-su-caducidad.html