Houses already exceed bubble costs and consultants consider they are going to rise extra | Economy | EUROtoday

Housing costs are gaining inertia once more and lots of consultants consider that the change in financial coverage of the European Central Bank will enhance them much more sooner or later, dangerous information for the hundreds of people that need (and infrequently can not) purchase a home in Spain. According to the newest knowledge from the National Institute of Statistics, quantities grew by 6.3% within the first quarter of this yr in comparison with the identical interval in 2023. This is a transparent acceleration: costs had been progressing under for 4 quarters of 5%.

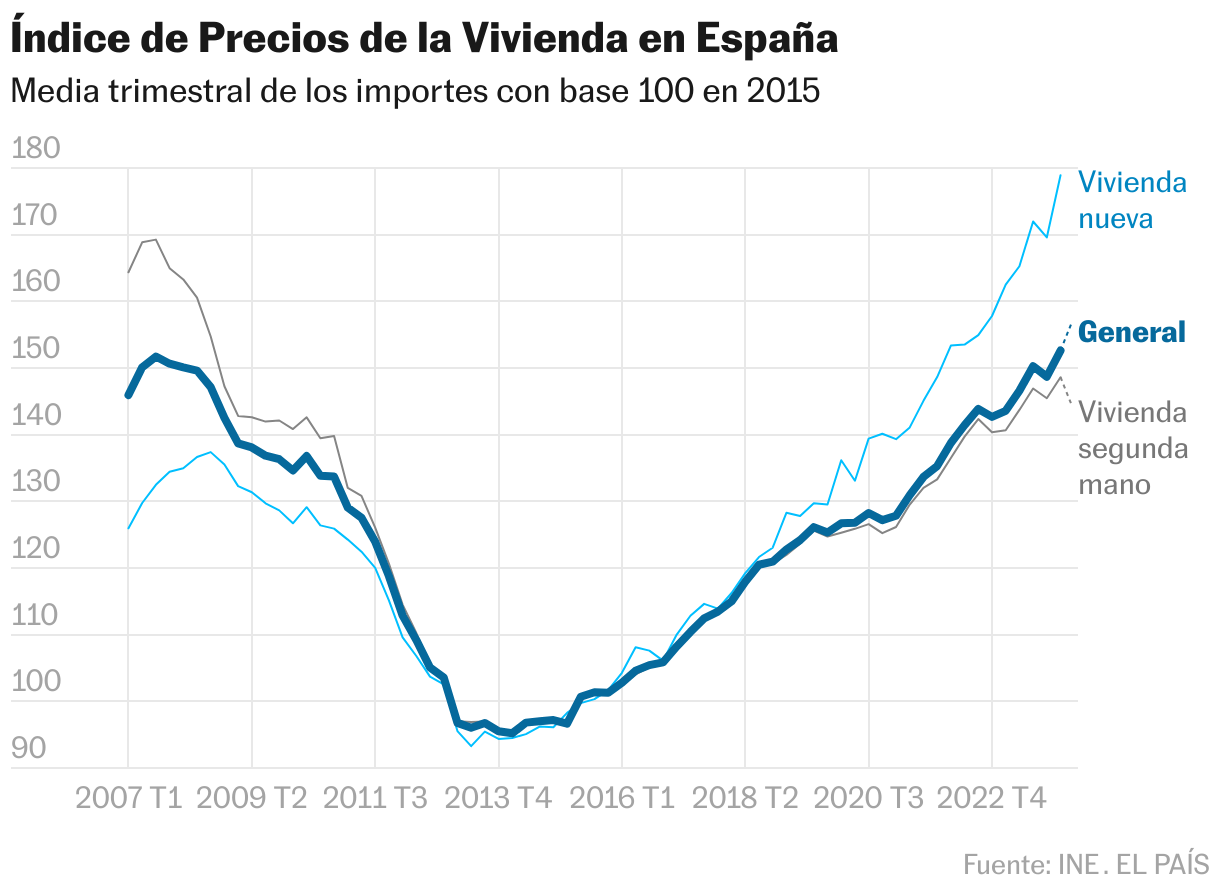

As a results of this pull, homes are dearer than ever. The official statistics, printed this Thursday, include a base index of 100 that takes as a reference what a house was price in 2015. Now this indicator exceeds 152 factors, which signifies that residences are 52% dearer than 9 years in the past. again. But the mark can also be a milestone, since for the primary time the 151.7 factors that till now represented the climax of the actual property bubble in the beginning of the century, akin to the third quarter of 2007, are exceeded.

Unlike then, new houses at the moment are rather more costly (nearly 179 factors), whereas second-hand houses are extra contained (148.6 factors). But that doesn’t forestall the truth that, between January and March, each sorts noticed their costs rise sharply. In model new residences, the development was double digits (10.1%) whereas the rise within the value of used housing remained at 5.7%. By autonomous neighborhood, the quantities made their largest bounce within the first quarter of the yr in Andalusia (7.9%), Navarra (7.6%) and La Rioja (7.1%). The improve in costs occurred in all territories, however in Castilla-La Mancha (4.7%), Asturias and Galicia (each with 5.1%) it was extra reasonable.

“The data confirm that the low supply in the market does nothing more than push prices up,” says Francesc Quintana, CEO of the actual property firm Vivendex. Quintana displays the sentiment of the sector, which attributes the escalation of housing, which has risen steadily since 2014 (within the INE sequence, it didn’t even go down in the course of the pandemic), to the robust imbalances between a scarce provide and a strong demand. After ten years of will increase, extra impetuous in some instances and extra discreet in others, costs appear removed from calming down.

To the despair of many households, consultants predict that the alternative will occur and the tempo at which housing grew between January and March might be maintained, and even acquire power, within the the rest of the yr. In the background lies the assumption that the development of homes will proceed to be scarce in relation to a requirement that’s fueled by the nice efficiency of the labor market and the nice expectations of the Spanish financial system. And added to that, this Thursday the European Central Bank (ECB) introduced the primary drop in official rates of interest in a very long time, which represents an inflection within the restrictive coverage that it inaugurated in 2022 to answer the inflationary disaster. “The de-escalation of interest rates will mark another year of significant increases in housing prices,” summarizes the Head of Studies at Fotocasa, María Matos.

Like yours, many analyzes despatched to the media after the INE knowledge grew to become identified affect that concept. Ferran Font, from the Pisos.com portal, additionally places it black on white: “Both the lack of supply and the ECB's rate policy will place us in a scenario in which, most likely, housing will increase its value more what he did last year,” he says.

Although mortgages will not be straight listed to the charges set by the ECB, they have a tendency to observe the identical developments. And cheaper mortgages imply extra demand and due to this fact extra room to boost costs. Patricia Rodríguez-Lázaro, head of the Investment division at Clikalia, predicts, for instance, “the beginning of a period of increases” in costs. “The growth reported by the INE does not completely reflect the high increases that we see daily in the sale and purchase of homes, where the increases reach double-digit figures,” she says, alluding to the developments that the corporate observes in cities corresponding to Madrid or Barcelona. .

A dilemma for patrons

Also at Don Piso they consider that the drop in charges, with its foreseeable reducing of loans, “will cause an increase in interest in purchasing homes.” The deputy basic director of the actual property company recommends to “anyone who wants to buy not to wait” if they will accomplish that with out resorting to a mortgage, as a result of “those who are waiting to buy at lower rates may end up paying the same.” That is, what they save by having a decrease rate of interest could not compensate within the month-to-month fee for the truth that the mortgage principal is larger.

The optimistic half is that the anticipated cheaper mortgages will certainly present aid to those that have already got one. That is what Javier Kindelan, director of Living (residential sector) at CBRE Spain, highlights: “People now find it more difficult to pay mortgages and we have seen that in the accessibility ratios.” The consulting agency estimates that households at present dedicate a mean of 39% of their earnings to paying for his or her dwelling. “The drop in the Euribor [el indicador de referencia de la mayoría de hipotecas variables] It will increase liquidity and reduce this burden a little,” completes the guide, who additionally believes that the brand new scenario will appeal to extra patrons, each on the a part of skilled funding and people, to the market.

This is now supported, in accordance with Matos, by a “solvent, purchasing power, investor and also foreign” demand that may purchase “without being intimidated due to high interest rates.” That is what explains for a lot of analysts that, regardless of the extraordinary rise in credit score costs since mid-2022 and the truth that fewer homes are offered, the quantities haven’t eased and are leaving an increasing number of households out of the housing market. “Prices, both for purchase and rental, are increasingly higher,” remembers Quintana, from Vivendex, who fears that the scenario will change into persistent: “This is going to create a situation of great social tension,” he predicts.

Follow all the data Economy y Business in Facebook y Xor in our e-newsletter semanal

Subscribe to proceed studying

Read with out limits

_

https://elpais.com/economia/2024-06-07/las-casas-ya-superan-los-precios-de-la-burbuja-y-los-expertos-creen-que-van-a-subir-mas.html