The financial system, a brand new ally earlier than Trump | Business | EUROtoday

Once once more, US President Donald Trump seems to have backtracked. The narrative flip has coincided with the sending of European troops to the Arctic territory and Brussels’ announcement of a battery of tariffs in retaliation for the tried annexation of Greenland. But these components haven’t been probably the most decisive, since they weigh little within the face of energy asymmetries and the tenacious European fragmentation that hinders any determination.

It is the markets that, as occurred after the so-called “liberation” day, have acted as firewalls to subdue the unilateralism of the main world energy. This week, unequivocal indicators of an tried monetary shock multiplied: sudden depreciation of the greenback, fall on Wall Street and, coincidentally, lack of investor confidence within the high quality of the US Treasury debt.

Such a wake-up name has motivated the United States to maneuver away from probably the most radical options, opening itself to negotiations. However, the battle has not disappeared and the result continues to be unsure, however its ins and outs present related classes for European and Spanish financial coverage.

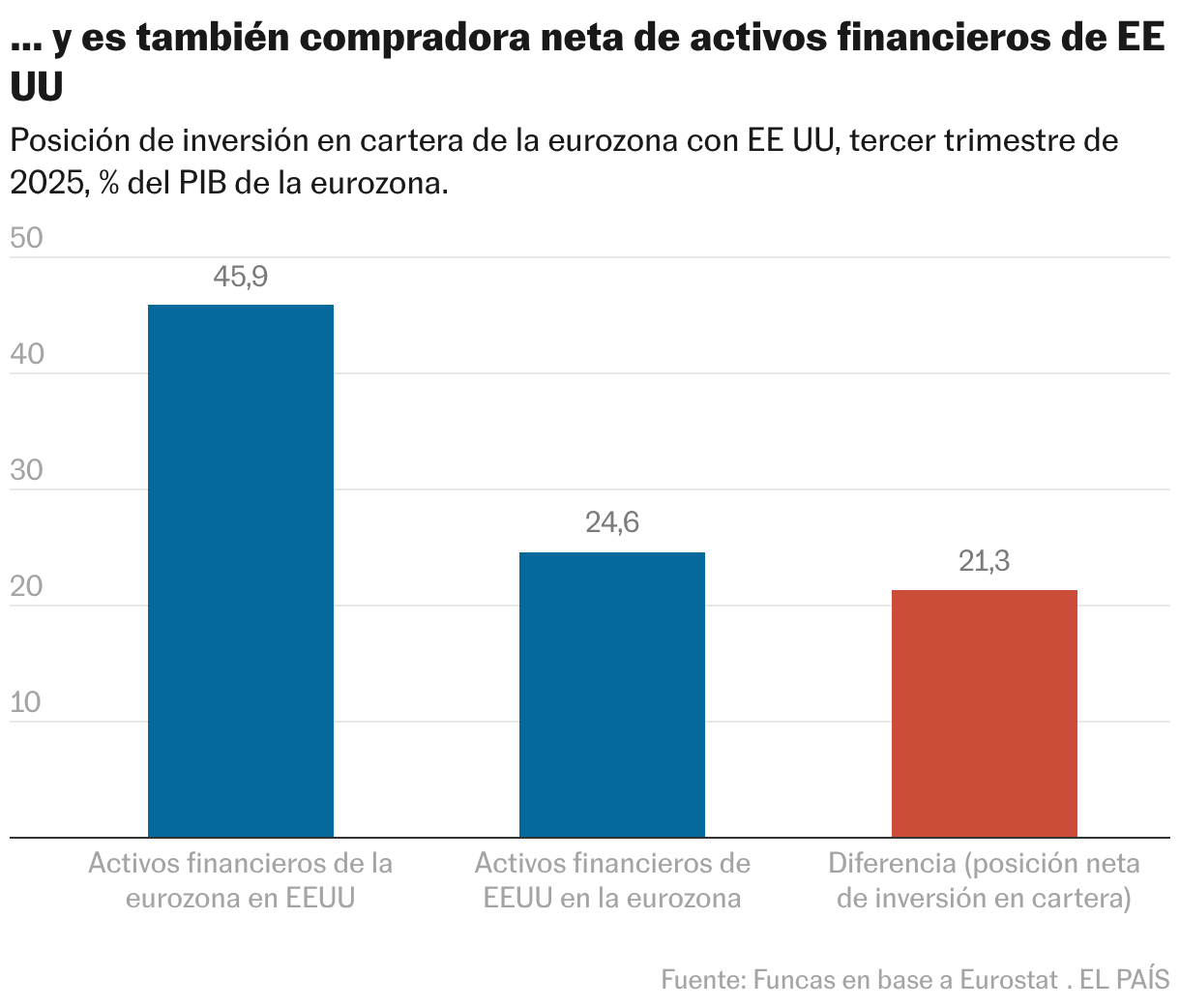

Firstly, it’s already proof that the monetary stability of the United States is determined by the goodwill of international savers, amongst whom Europeans stand out. The amassed quantity of assets invested by Europe within the monetary markets of the principle world energy, or portfolio funding place, exceeds 7.2 trillion euros, that’s, virtually 46% of the GDP of the eurozone. The Spanish portfolio, though not the principle one, quantities to 127,000 million. Conversely, the influx of portfolio funding from the US doesn’t attain 4 billion euros, so the online place is 3.2 billion in favor of Europe. This clearly favorable stability, revealing the dependence on the skin to finance the big ball of public debt that’s accumulating on the opposite facet of the Atlantic, has emerged as an efficient lever to constrain the motion of the Republican government.

Now, and it is a second lesson, we should not overestimate our deterrent capability in monetary issues, since Europe suffers from a scenario of extra financial savings in comparison with the weak point of funding: by definition, this imbalance brings with it an outflow of capital to different locations. Therefore, the underlying drawback lies within the lack of funding and dynamism of the neighborhood bloc, one thing that can not be solved by the ravings of the United States. In the absence of initiatives and reforms that enhance funding each on the European stage and in every nation – additionally in Spain – we are going to proceed to lose financial savings inexorably. Going deeper, the weak point of funding comes primarily from the personal sector, for the reason that public has elevated its contribution, notably in Spain.

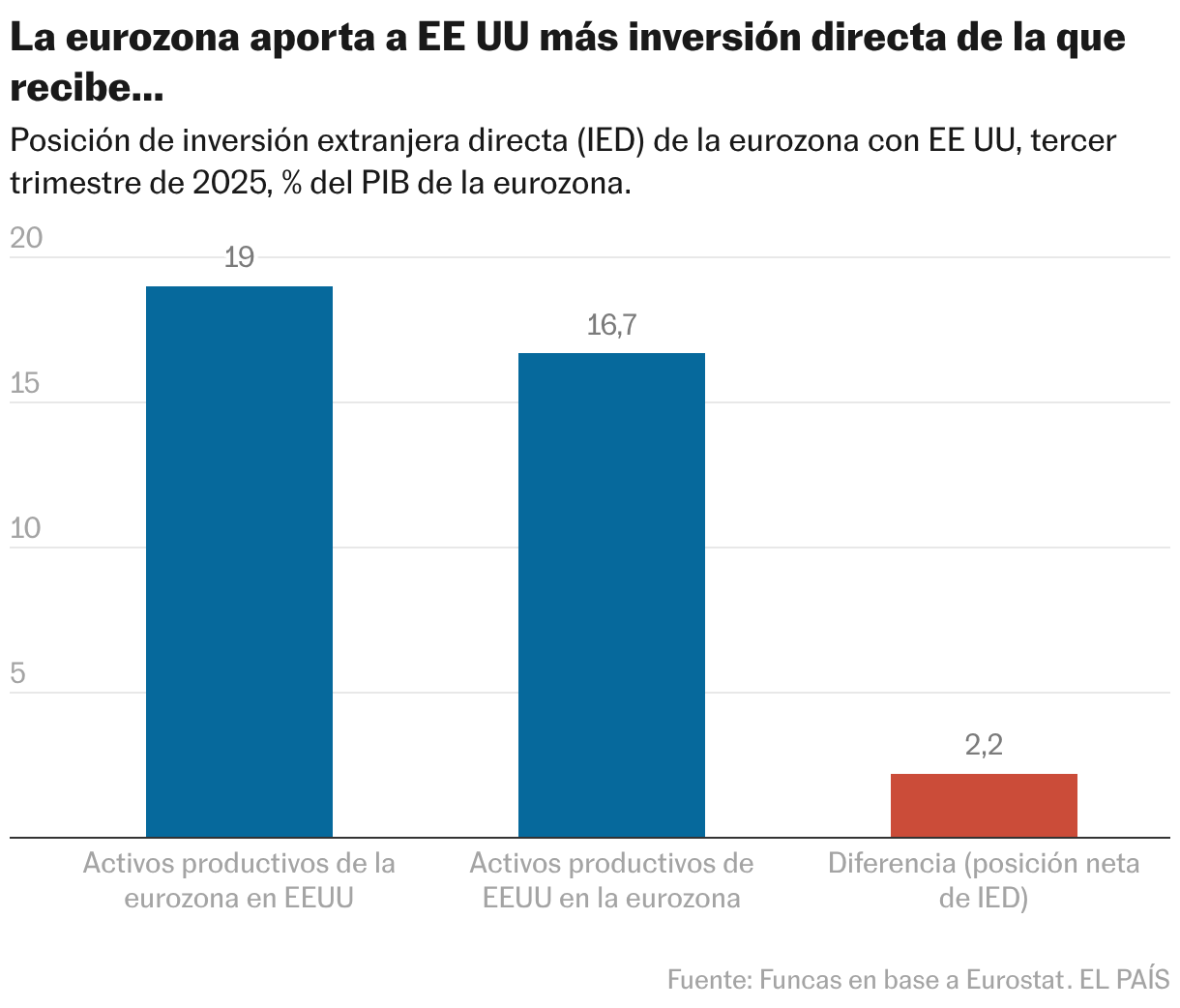

The outflow of international direct funding is one other symptom of the imbalance. The quantity of productive belongings amassed by European firms in North American territory now exceeds three trillion euros, in comparison with 2.6 trillion in the other way, in order that the online place is equal to 2.2% of the Community GDP. The identical scenario of direct funding outflow prevails in Spain, with a good larger internet place of three.2% of GDP. In different phrases, Europe invests extra within the productive material of the world’s main energy than it receives.

For now, neither Trump’s tariffs nor the market containment dam have altered this cussed actuality. The excellent news is that the Spanish financial system is holding up nicely in such a fancy geopolitical context. The problem continues to be the shortage of consensus to confront inner challenges and strengthen the European response to a moribund multilateral system.

Balance

The surplus of the Spanish exterior accounts is maintained regardless of the buildup of adversities such because the tariff conflict, the languor of the European market or the deterioration of competitiveness entailed by the inflation differential in comparison with the euro zone. The present account stability – which data the distinction between earnings from overseas and funds – confirmed a constructive stability till October near 47,000 million euros, this being the most effective determine for this era within the historic collection. The strong surplus of tourism and non-tourism companies has been a key issue on this outcome.

https://elpais.com/economia/negocios/2026-01-25/la-economia-nuevo-aliado-ante-trump.html