The OECD warns of a brand new improve in private revenue tax in Spain because the tax doesn’t adapt to inflation | Economy | EUROtoday

The tax burden on employees elevated once more in many of the world’s superior economies final 12 months. It did so, to a big extent, routinely and silently, within the warmth of rising costs. This is confirmed by the Organization for Economic Cooperation and Development (OECD) in its report Taxing Wages 2025printed this Wednesday. Spain, based on the group, didn’t escape the pattern and the non-public revenue tax (IRPF) routinely turned dearer as a result of the tax system didn’t alter to the tempo of inflation.

This phenomenon, technically referred to as chilly progressivity, seems when nominal wages rise to attempt to compensate or alleviate the rising value of life. In these instances, when the tax brackets and deductions stay unchanged, the employee finally ends up leaping to a better tax step or paying a better proportion of his wage with out his actual buying energy bettering in the identical proportion.

The OECD presents information for instance the change. In 2025, the typical gross wage in Spain stood at 32,678 euros, which represents a rise of three.8% in comparison with the earlier 12 months. At first look, a mean employee gained the battle towards costs, since inflation was 2.6%, permitting an enchancment in gross buying energy of 1.2 factors. However, the typical private tax charge borne by the taxpayer elevated by 1.5%, thus absorbing the achieve.

The key indicator to measure this phenomenon is what the OECD calls the “fiscal wedge.” It is an idea historically utilized by the group with the intention of exhibiting the distinction between the full labor prices for the employer (gross wage plus firm contributions) and the online wage obtained by the worker (after deducting private revenue tax and contributions payable to him). This indicator is mostly expressed as a proportion of labor prices.

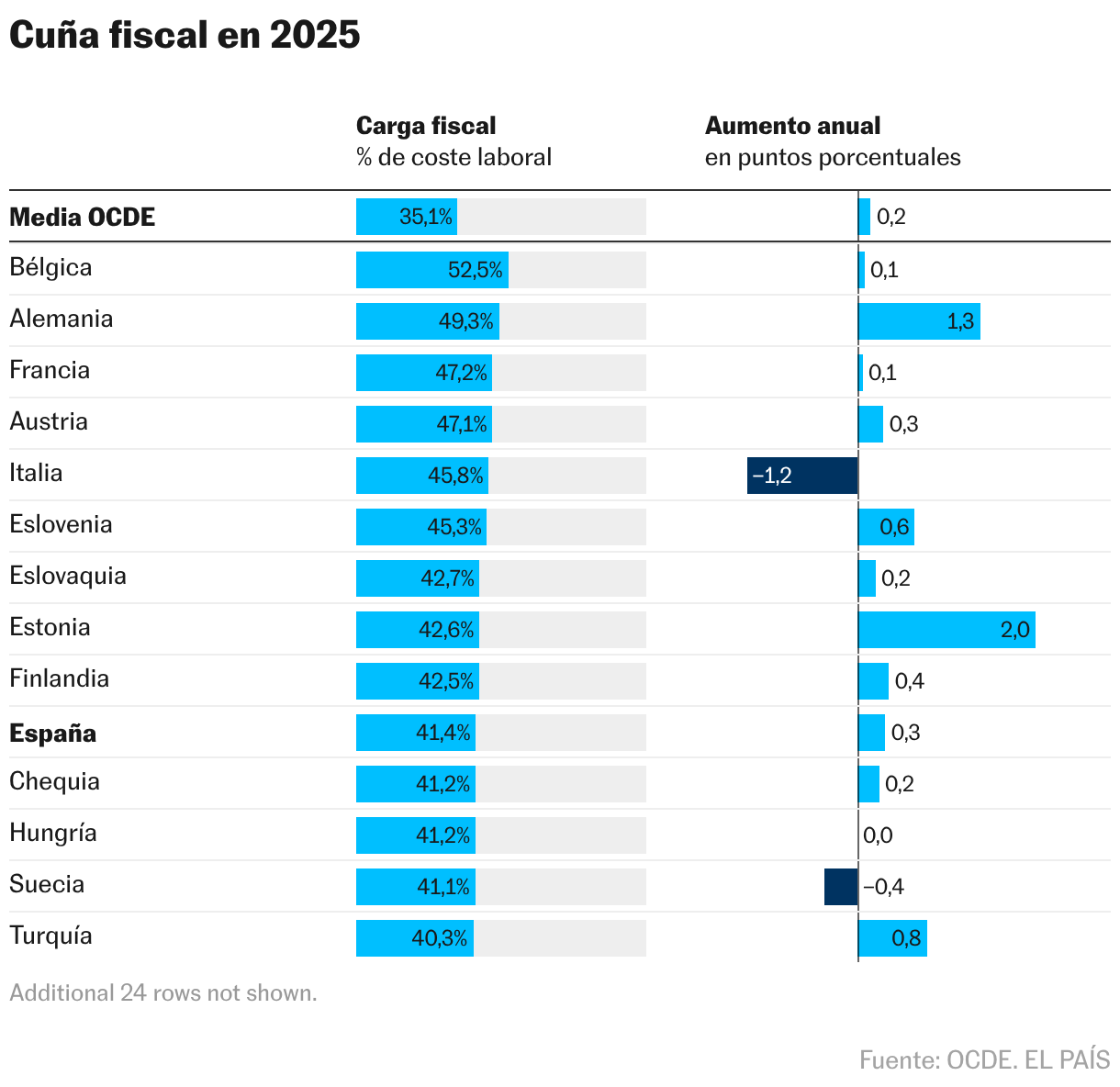

In Spain, for a single employee with a mean wage, the tax wedge rose to 41.4% in the course of the 12 months, 0.3 factors greater than the earlier 12 months and effectively above the OECD common, which remained at 35.1%. The report explains that non-public revenue tax contributed 0.25 factors to this improve, whereas the social contributions paid by the corporate rose 0.05 factors. In this final part, the Intergenerational Equity Mechanism (MEI) performs a figuring out position, an extra contribution launched to assist pensions that the research particularly mentions as a rise issue.

Spain will not be alone on this pattern, because the tax burden rose in 24 of the 38 OECD nations for the fourth consecutive 12 months. In the United Kingdom, for instance, essentially the most drastic improve within the bloc was recorded (2.45 proportion factors), exactly as a result of revenue tax thresholds have been frozen whereas salaries rose nominally. Estonia (1.94 factors) and Germany (1.34 factors) additionally registered hanging will increase, whereas within the OECD common the rise was 0.15 factors.

When breaking down the Spanish system, the report particulars that the best weight of labor taxes falls, as has been the case for years, on Social Security contributions paid by the corporate, which signify 23.4% of complete labor prices, a determine that’s effectively above the typical of the nations that make up the bloc, of 13.5%. Next is private revenue tax, with a weight in Spain of 13.1%, on this case under the typical of the membership that brings collectively wealthy economies (13.4%). Finally, there are the contributions of the employee himself (5% in Spain and eight.1% within the OECD common).

More progressivity on the backside

The report additionally sheds gentle on some particularities that make Spain a system of contrasts, particularly in the way it encourages or penalizes elevated revenue. A notable facet is the trouble to guard those that enter the labor market with modest salaries by the discount for acquiring revenue from work. This measure, which in 2025 has been strengthened for internet incomes of lower than 19,747 euros per 12 months, causes a really sharp improve in progressivity within the first revenue bracket. Thanks to this, Spain is among the OECD nations the place progressivity will increase most abruptly originally of the wage scale, as acknowledged by the group.

In truth, the tax wedge for single employees with out youngsters will increase progressively as revenue will increase: it stands at 37.9% for many who earn 67% of the typical wage, rises to 41.4% for the typical wage and reaches 46.2% for increased incomes situated at 167% of the nationwide common.

However, the research additionally warns that in Spain, as in different developed nations, there are vital factors the place the employee faces efficient marginal charges in sure sections of his revenue that may escalate as much as 70% and which are defined as a result of, by incomes just a little extra money, the taxpayer concurrently loses the fitting to obtain social help or tax deductions linked to the extent of revenue.

On the opposite, the Spanish system presents a really totally different conduct on the highest revenue ranges as a result of impact of contribution ceilings. Unlike what occurs in different nations, in Spain contributions to Social Security don’t develop indefinitely with wage, however fairly have a most ceiling set at 58,914 euros per 12 months for 2025. From this threshold, the marginal charge of contributions all of the sudden falls, which causes the system to lose redistributive pressure on the high of the desk.

https://elpais.com/economia/2026-04-22/la-ocde-advierte-de-una-nueva-subida-del-irpf-en-espana-al-no-adaptarse-el-impuesto-a-la-inflacion.html