The rise in fuel and the danger of recent tariffs threaten the truce in inflation | Economy | EUROtoday

The pax financial system faces its first assaults of the 12 months. In the 2026 script, a return of tariffs didn’t seem as a central risk. Much much less that his return was linked to the expansionist ambition of the United States in Greenland. Although after the storm that the tariffs unleashed in April, and given the fragility of Donald Trump’s phrase, it was not a far-fetched state of affairs for him to make use of the protectionist wild card once more, nor would it not be a brand new, umpteenth, retreat from the US president, an element of fixed uncertainty for the worldwide economic system.

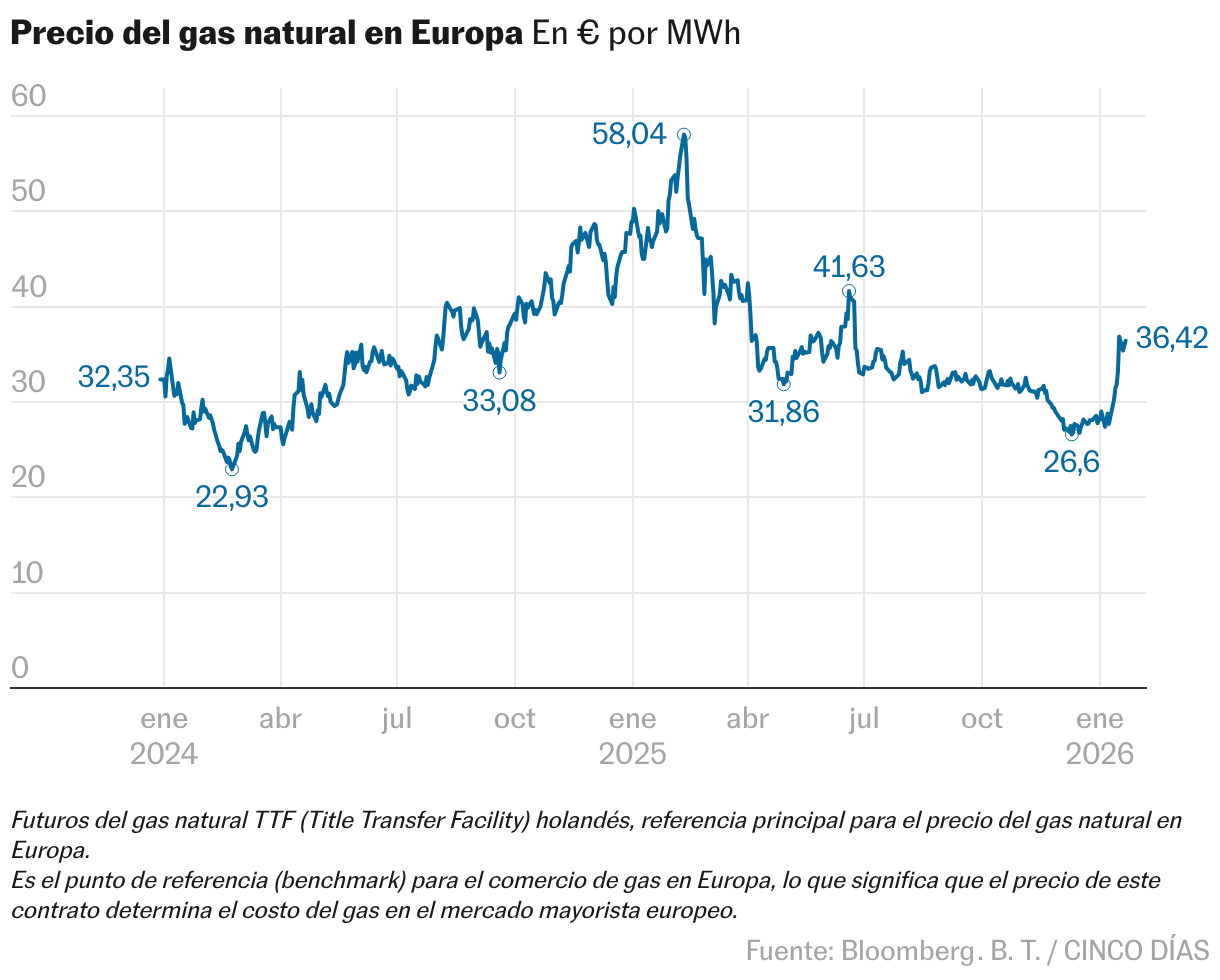

The risk of extra 10% levies by Washington on merchandise from Denmark, Norway, Sweden, France, Germany, the United Kingdom, the Netherlands and Finland as of February 1 – extendable to 25% from June if there isn’t any progress -, along with the response ready by the European Union, and the rise of round 30% to date this 12 months within the worth of pure fuel within the Dutch TTF market, have altered a begin to the 12 months that was appeared placid for the European Central Bank. Inflation in December was slightly below the goal, at 1.9%, and rates of interest are set at a cushty 2%.

It can’t be stated, nonetheless, that each phenomena will probably be adequate to trigger an inflationary reactivation. Natural fuel began from a really low worth threshold, and its fast development has returned it to August ranges, above 35 euros per megawatt hour, however nonetheless virtually 30% beneath the January 2025 ranges.

Norbert Rücker, director of Economic Research on the Swiss financial institution Julius Baer, believes that behind the violent rise in pure fuel there could also be larger warning amongst buyers who have been betting on its fall, who worry that they’ve gone too far. “The intensity of the price rally in recent days points to a wave of profit-taking in the futures market, especially since sentiment had been quite bearish previously,” he notes. Another analyst, Juan Ignacio Crespo, sees its upward evolution as pure, because it brings European fuel nearer to cost convergence with fuel from the United States, from which it was separated final August.

The European Union started the winter with fuel reserves barely above 82%, the bottom determine because the begin of the vitality disaster and the second lowest in a decade. Although the proportion could seem excessive, it was ten factors beneath the historic common, in a collection that begins in 2011, which has not helped hold its worth low. Its evolution because the chilly and heating stage progresses has not recovered: the determine has dropped to round 50.4% of capability, decrease than the 61.7% of a 12 months in the past.

Retaliation

Regarding tariffs, the ECB sees two-way dangers to inflation. At his final assembly, he repeated the same old message that inflation may very well be decrease if rising US tariffs cut back demand for euro zone exports. In reality, early estimates from Bloomberg economists recommend that Trump’s tariffs, together with the prevailing charges and the extra 10%, might cut back the exports of affected international locations by as much as 50% in comparison with their pre-2025 ranges.

However, the commerce retaliation being ready by Brussels was not on Frankfurt’s radar on the time, and has the potential to push costs up on the continent. Christine Lagarde herself has warned on a number of events that it’s the European utility of tariffs in response to Trump, and never these utilized by Washington, that may elevate European inflation.

The final time was in September, when he acknowledged that almost all Eurobank fashions contemplated that, if reciprocal tariffs have been utilized, import prices would enhance and provide chains can be affected, inflicting a rise in inflation within the quick time period. That risk is not fiction: the European Union is contemplating hitting US merchandise with tariffs price 93 billion euros if Trump doesn’t rectify it.

Agathe Demarais, a geoeconomics knowledgeable on the European Council on Foreign Relations (ECFR), a pan-European suppose tank, believes that Washington’s intimidation is watered down: Trump’s failure to increase tariffs to your complete EU leaves room for firms to keep away from them. “The US tariff threats are directed at only six EU countries, meaning they would not be difficult to circumvent within the Single Market (Belgium borders France, Germany and the Netherlands).”

And he insists on the concept that the most important losers would be the North American residents themselves. “US tariffs are a tax on their own companies and consumers: US importers absorb 96% of tariff costs,” he factors out. The inflationary blow to the EU, due to this fact, would come solely from the quantity of group retaliation towards the United States.

Given the precedents of Trump’s modifications of opinion, the markets don’t absolutely imagine that the state of affairs will degenerate into a significant shock that forces central banks to recalculate their rate of interest actions. The European inventory markets turned pink on each Monday and Tuesday – amongst them the French champagne producers, threatened by Trump with a 200% tariff – however there was no crash of the proportions of final April, when the commerce warfare broke out, and the principle indices stay near historic highs. The Euribor doesn’t but replicate worry of worth will increase that may elevate mortgage funds, and futures don’t low cost rate of interest will increase or decreases by the European Central Bank in 2026.

Spain, extra protected

In the precise case of Spain, Raymond Torres, director of Economics at Funcas, believes that it’s early to attract conclusions, however whereas he considers that the impression for Spain of a tariff escalation can be comparatively small attributable to little publicity to the United States, he does see extra causes for concern within the vitality discipline. “Gas is what may be the most worrying, because it represents 1% of the CPI, and influences the formation of the price of electricity, which could increase inflation by a few tenths, although gas prices are very volatile, and although it has risen abruptly in price, it can also fall just as quickly,” he factors out.

For economist Javier Santacruz, this damaging information might delay the normalization of costs in Spain, the place inflation closed December at 2.9%. “Both gas and cross tariffs in the very short term will reduce the chances of the inflation rate slowing down, especially for Spain, which will keep it above what we expected. I don’t think it will accelerate inflation, but it will hinder the rate from slowing down,” he predicts.

https://elpais.com/economia/2026-01-21/la-subida-del-gas-y-el-riesgo-de-nuevos-aranceles-amenazan-la-tregua-de-la-inflacion.html